Education Loan for Engineering Students in Karnataka — Banks, Interest Rates and College-Wise Guide

You've got a KCET or COMEDK seat, the college says pay Rs 1.5 lakh by Friday, and your family doesn't have that much ready cash. Here's the answer you need right now: any AICTE-approved Karnataka engineering college qualifies for education loans from public sector banks at 8-10% interest, loans under Rs 7.5 lakh don't require collateral, and you can apply through the Vidyalakshmi portal to reach multiple banks with a single application.

But that's just the starting point. The real questions Karnataka families face are more specific: which bank actually approves loans for your particular college? How much can you borrow for a private management quota seat versus a government quota seat? Are there government schemes that cover fees entirely so you don't need a loan at all? And what happens to repayment if placements don't work out? This guide answers all of these based on what we've been tracking through CollegesInfo.org since 2019.

Do You Actually Need a Loan? Check Karnataka Government Schemes First

Before borrowing, check whether you're eligible for fee coverage that doesn't require repayment. Karnataka has some of the strongest scholarship programmes in India for engineering students, and many families don't know about them — or find out too late.

SSP (Student Scholarship Portal) Karnataka

The SSP Karnataka scholarship covers tuition fees for SC, ST, OBC, and minority students at government and private colleges. If your family income is below the threshold (varies by category — roughly Rs 2.5 lakh for SC/ST, Rs 1 lakh for OBC), SSP can cover your entire engineering tuition. That's a complete substitute for a loan, not just a discount. Apply through ssp.postmatric.karnataka.gov.in within the deadline — usually September-October after the academic year starts.

Vidyasiri Scholarship

Vidyasiri covers OBC students specifically, with income limits around Rs 1 lakh per year. It covers tuition and a maintenance allowance. If you're OBC and your family income qualifies, you shouldn't be taking a loan at all — Vidyasiri plus the fee waiver at government colleges means your B.Tech could cost nearly zero out of pocket.

Central Sector Scheme (MHRD)

The central government's post-matric scholarship covers students from all categories who scored above 80th percentile in their Class 12 board exams. It's not Karnataka-specific, but Karnataka students are eligible. The amount isn't as large as SSP — typically Rs 10,000-20,000 per year — but it reduces the loan amount you'd need.

How Education Loans Work for Karnataka Engineering Colleges

The basic structure is the same across all banks: you borrow the amount needed for tuition, hostel, and related expenses; the bank charges interest during the course (which you can optionally pay as it accrues, or let it add up); after graduation you get a 6-12 month grace period; and then you repay in EMIs over 5-15 years. The differences between banks come down to interest rates, maximum loan amounts, collateral requirements, and — critically — which colleges they're willing to lend for.

Collateral Rules (RBI Guidelines)

This catches many families off guard. Under RBI guidelines, loans up to Rs 7.5 lakh don't require any collateral — just a co-borrower (usually a parent). Between Rs 7.5 lakh and Rs 20 lakh, banks typically ask for a third-party guarantee or modest collateral. Above Rs 20 lakh, property collateral is usually mandatory. Since most Karnataka engineering courses through KCET government quota cost Rs 2-6 lakh total over 4 years, the majority of KCET students won't need collateral at all.

Management quota is where it gets expensive. A management quota seat at RVCE or MSRIT through COMEDK can cost Rs 8-12 lakh total, which crosses the collateral-free threshold. Private colleges like PES University with fees of Rs 3-4 lakh per year definitely need the collateral conversation with your bank.

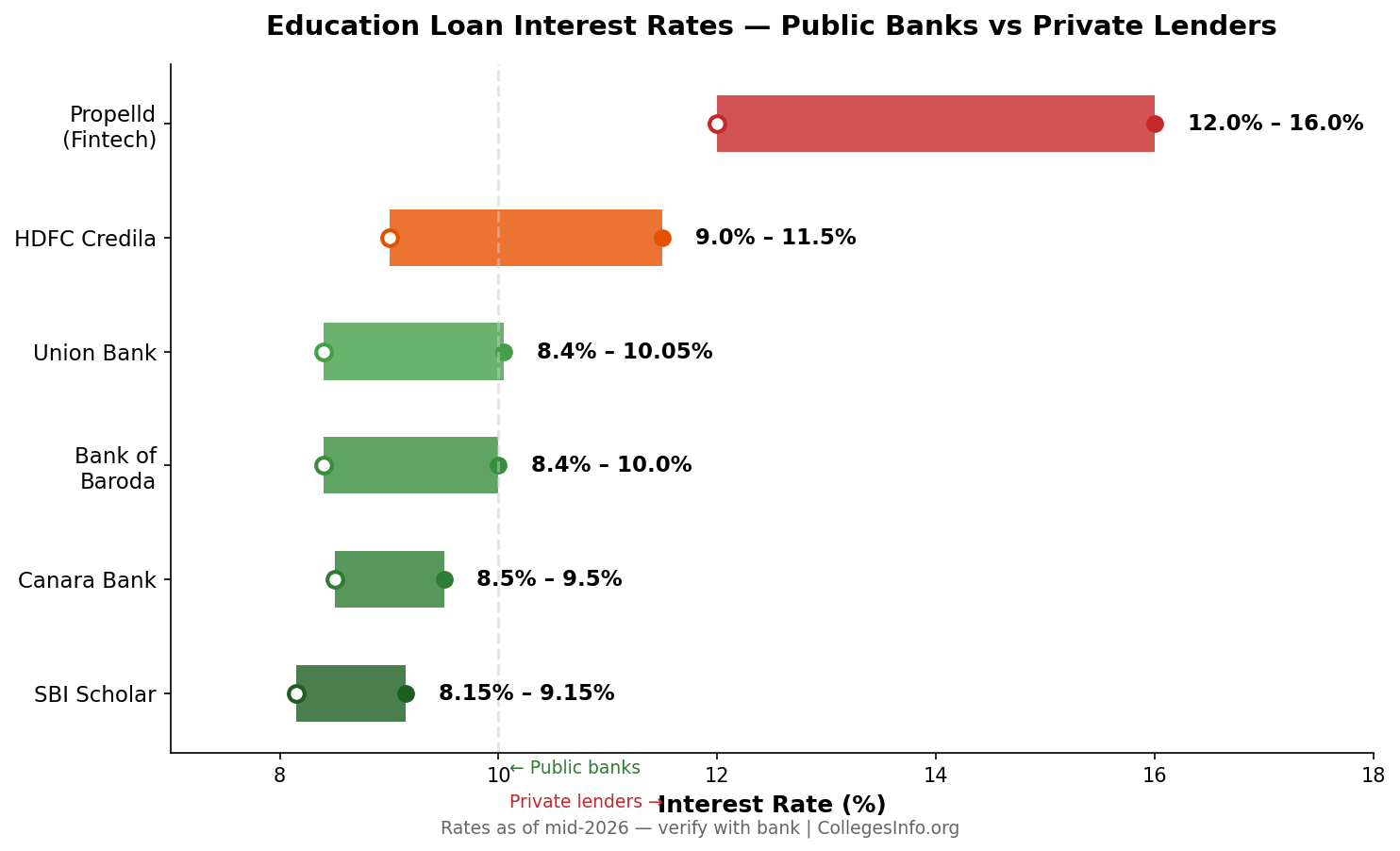

Interest Rate Structure

Public sector banks (SBI, Canara Bank, BOB, Union Bank) offer the lowest rates — typically 8-10% for domestic courses. Private banks and NBFCs (HDFC Credila, Avanse, Propelld) are faster to approve but charge 10-16%. The difference matters enormously over a 7-10 year repayment period. On a Rs 8 lakh loan, the difference between 8.5% (SBI) and 14% (fintech lender) is roughly Rs 2.5 lakh in extra interest over the loan tenure. Always try public sector banks first.

One important detail: girl students get a 0.5% concession at most public sector banks. This isn't widely advertised but it's standard RBI-recommended practice. Ask specifically when applying.

Which Banks Approve Loans for Which Karnataka Colleges?

This is the question no other guide answers properly, and it's the one that matters most to families. Banks don't treat all colleges equally. Here's how the approval tiers work in practice.

Tier 1 Colleges — Approved Instantly by All Banks

RVCE, BMSCE, PES University, MSRIT, NIE Mysuru, NITK Surathkal — any NAAC A-grade or above college with strong placement records gets approved by every bank without hesitation. Loan processing takes 5-10 days. These colleges often have tie-ups with specific banks that offer reduced documentation.

Tier 2 Colleges — Approved by Most Banks

DSCE, NHCE, CMRIT, RNSIT, AIT, SIT Tumkur, BIT Bangalore — NAAC B+ or above colleges with reasonable placement track records. Public sector banks approve these readily. Private lenders approve these too but may charge slightly higher rates. Processing takes 10-20 days. If a bank hesitates, it's usually a documentation issue, not a college-quality issue.

Tier 3 Colleges — Selective Approval

Smaller private colleges without NAAC accreditation, or with NAAC B or below, face tougher loan approvals. Public sector banks may still approve if the college is AICTE-approved and VTU-affiliated, but they'll require more documentation and may ask for collateral even below Rs 7.5 lakh. This is where fintech lenders like Propelld or Avanse become useful — they're less concerned about college tier and more about the student's admission confirmation.

A Practical Tip

Before committing to a college, call the bank's education loan desk and confirm they'll lend for that specific institution. Don't assume approval based on general eligibility. Some banks maintain internal lists of approved colleges, and if your college isn't on the list, the process becomes significantly slower.

The Vidyalakshmi Portal — How to Apply to Multiple Banks at Once

The government's Vidyalakshmi portal lets you submit one application that goes to up to three banks simultaneously. It's the fastest way to compare offers and avoid running around to bank branches. Here's how to use it effectively.

Register with your Aadhaar, PAN, and college admission letter. Select your course and college from the dropdown (most VTU-affiliated colleges are listed). Choose up to three banks — we'd recommend selecting SBI Scholar Loan, Canara Vidya Turant, and Bank of Baroda as your three, since these have the best combination of low rates and Karnataka-specific familiarity. You'll hear back from each bank within 7-10 working days. Compare the offers on interest rate, processing fee, and repayment flexibility before accepting.

Government Quota vs Management Quota — The Loan Difference

This is where many families miscalculate. The same college can have drastically different fee structures depending on which quota you're admitted through, and that directly affects your loan amount and approval difficulty.

| Factor | KCET Govt Quota | COMEDK/Mgmt Quota |

|---|---|---|

| Annual fee (typical) | Rs 45,000–1.2 lakh | Rs 1.5–3.5 lakh |

| 4-year total cost | Rs 1.8–5 lakh | Rs 6–14 lakh |

| Loan needed? | Often no (scholarship covers) | Usually yes |

| Collateral needed? | No (under 7.5L) | Maybe (if above 7.5L) |

| Bank approval speed | Fast (3-7 days) | Moderate (10-20 days) |

The takeaway: if your KCET rank gets you a government quota seat, that's almost always better financially than a COMEDK management quota seat at the same college. You're getting identical education and placement access at Rs 4-8 lakh less over four years. That's the equivalent of the difference between needing a loan and not needing one at all.

Interest Subsidy Schemes — Getting the Government to Pay Your Interest

Two central government schemes can cover your loan interest entirely during the course period — effectively making your loan interest-free while you study.

Central Government Interest Subsidy Scheme (for Economically Weaker Sections)

If your family's annual income is below Rs 4.5 lakh, the central government pays the interest on your education loan during the moratorium period (course duration + 1 year). This means you only start paying interest after your grace period ends — by which time you should be employed. The bank handles the subsidy claim; you don't need to apply separately, but you do need to provide income proof at the time of loan application.

State-Level Schemes

Karnataka's Department of Minorities Welfare and Backward Classes Welfare departments offer additional interest subsidy schemes for SC/ST/OBC students. These stack with the central scheme in some cases. Check with your district commissioner's office or the Karnataka scholarships guide for the specific scheme applicable to your category.

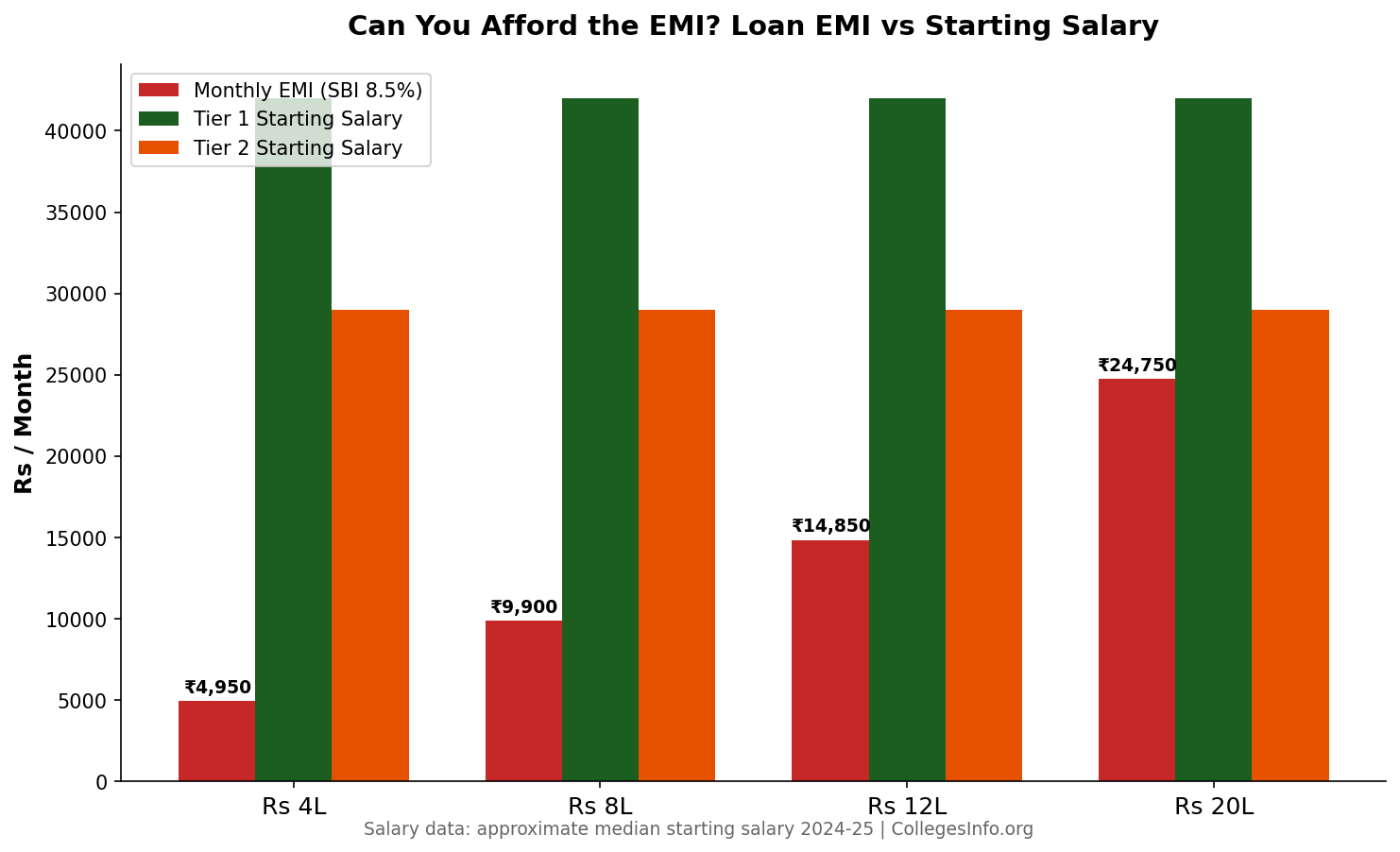

Repayment Reality Check — What EMIs Look Like After Graduation

The part nobody talks about honestly. Here's what your monthly EMI looks like for typical Karnataka engineering loan amounts, assuming a 10-year repayment tenure at different interest rates.

| Loan Amount | EMI at 8.5% | EMI at 10.5% | EMI at 14% |

|---|---|---|---|

| Rs 4 lakh | Rs 4,950/mo | Rs 5,400/mo | Rs 6,220/mo |

| Rs 8 lakh | Rs 9,900/mo | Rs 10,800/mo | Rs 12,440/mo |

| Rs 12 lakh | Rs 14,850/mo | Rs 16,200/mo | Rs 18,660/mo |

| Rs 20 lakh | Rs 24,750/mo | Rs 27,000/mo | Rs 31,100/mo |

Context matters: the average starting salary for a CSE graduate from a Tier 1 Karnataka college is Rs 5-8 LPA (Rs 42,000-67,000 per month). From a Tier 2 college, it's Rs 3.5-5 LPA (Rs 29,000-42,000). An EMI of Rs 10,000-15,000 is manageable on a Tier 1 salary but tight on a Tier 3 salary. This is why the college you choose matters for loan decisions — it's not just about getting the degree, it's about whether the placement outcome supports the repayment.

Tax Benefits on Education Loans — Section 80E

Under Section 80E of the Income Tax Act, the interest paid on your education loan is fully deductible from your taxable income — with no upper limit — for up to 8 years from when you start repaying. Note that only the interest component qualifies, not the principal. This effectively reduces your real interest rate by your tax bracket. If you're in the 20% tax bracket and paying 9% interest, your effective rate drops to about 7.2%. This benefit applies to loans taken from banks and approved financial institutions — not from relatives or informal lenders.

Education Loan for Specific Karnataka Colleges — What to Expect

Different colleges mean different loan experiences. Here's what families typically face when applying for loans at specific Karnataka institutions.

RV College of Engineering and BMS College of Engineering

RVCE and BMSCE are on every bank's priority list. SBI processes loans for these colleges in 3-5 working days. The KCET government quota fee is roughly Rs 50,000-70,000 per year — most families don't even need a loan for this. It's the COMEDK management quota at Rs 2-3 lakh per year where loans become necessary. Both colleges have dedicated bank counters on campus during admission season.

PES University and MS Ramaiah Institute of Technology

PES University fees are higher than autonomous VTU colleges — Rs 2.5-4 lakh per year depending on branch and quota. Most families need a loan of Rs 8-12 lakh total. SBI and HDFC Credila both have tie-ups with PES. MSRIT has a similar fee structure for management quota, though KCET government quota is significantly cheaper at Rs 1-1.5 lakh per year.

Tier 2 Colleges — DSCE, NHCE, RNSIT, CMRIT

Loan approval is straightforward at all VTU-affiliated Tier 2 colleges. Fees range from Rs 1-2 lakh per year through KCET, meaning a total loan of Rs 4-8 lakh — well within the collateral-free limit. Processing takes 7-15 days at public sector banks. One tip: if you're applying at a college that's less well-known, bring the AICTE approval letter and NAAC certificate to the bank — it speeds up verification.

Regional Colleges Outside Bangalore

Colleges in Mysuru, Mangalore, Hubli, and Davangere have lower fees — often Rs 40,000-80,000 per year through KCET. Many students at these colleges don't need loans at all, especially if they qualify for SSP or Vidyasiri. For those who do need a loan, local branches of Canara Bank (headquartered in Mangalore) and Karnataka Bank are often faster than SBI for regional college applications.

Common Mistakes Karnataka Families Make With Education Loans

Mistake 1: Borrowing From a Fintech Lender Without Trying Banks First

Fintech companies (Propelld, Avanse, InCred) are aggressively marketed on campus and approved fast. But their interest rates are 12-16% versus 8-10% at public sector banks. On a Rs 8 lakh loan over 10 years, that's Rs 2-3 lakh extra in interest. Apply to SBI or Canara Bank first — yes, they're slower, but the savings are significant.

Mistake 2: Not Applying for Scholarships Before Taking a Loan

Many SC/ST/OBC families take Rs 4-5 lakh loans for engineering courses that SSP Karnataka would've covered entirely. The scholarship application deadline is usually October — months after the loan is disbursed. Apply for both simultaneously, and if the scholarship comes through, use it to prepay the loan.

Mistake 3: Ignoring the Moratorium Period Interest

During your 4-year course, interest keeps accruing. On a Rs 8 lakh loan at 9%, that's roughly Rs 3 lakh of accumulated interest by the time you graduate — turning your Rs 8 lakh loan into Rs 11 lakh. If your family can afford to pay even the interest during the course (Rs 5,000-6,000/month), it saves Rs 3 lakh in the long run.

Mistake 4: Choosing a College Based on Loan Availability Instead of Placement Quality

Some fintech lenders approve loans for colleges that public sector banks won't touch. That's a red flag, not a feature. If SBI won't lend for a particular college, there's usually a reason — poor accreditation, weak placement track record, or regulatory issues. The ease of getting a loan shouldn't override the quality of the college.

Step-by-Step: How to Apply for an Education Loan in Karnataka

Here's the practical sequence that works, based on what we've seen families do successfully.

Step 1: Get your admission confirmation letter from the college with the fee structure clearly stated. Banks won't process without this.

Step 2: Check SSP and Vidyasiri eligibility. If you qualify for full fee coverage, you may not need a loan at all.

Step 3: Register on the Vidyalakshmi portal and submit applications to SBI, Canara Bank, and one other bank of your choice.

Step 4: Simultaneously visit your nearest branch of your preferred bank with documents: admission letter, fee structure, Class 10 and 12 marksheets, KCET/COMEDK rank card, parent's income proof, identity documents, and two passport photos.

Step 5: Compare offers when they come back. Look at: interest rate, processing fee (should be zero or minimal for education loans), repayment tenure options, and any prepayment penalties.

Step 6: Accept the best offer. The bank disburses funds directly to the college — not to your personal account. You'll receive a disbursement schedule aligned with the college's fee payment deadlines.

Frequently Asked Questions About Education Loans in Karnataka

Can I get a loan for a COMEDK management quota seat?

Yes. Banks lend for management quota seats at AICTE-approved colleges. However, the higher fees mean you'll likely need a larger loan and potentially collateral if the total exceeds Rs 7.5 lakh.

What if my loan application is rejected?

Rejection usually means one of three things: your college isn't on the bank's approved list, your co-borrower's credit score is low, or your documentation was incomplete. Try a different bank — approval criteria vary. If multiple banks reject, fintech lenders like HDFC Credila or Avanse are more flexible but charge higher rates.

Is there a moratorium on education loan repayment?

Yes. You don't pay EMIs during your course. Repayment starts 6-12 months after course completion or after you get a job, whichever comes first. Interest does accrue during this period though.

Can I prepay my education loan without penalty?

RBI guidelines prohibit prepayment penalties on floating-rate education loans from banks. So yes — if you get a good placement and want to close the loan early, you can do so without extra charges. This doesn't always apply to NBFC lenders — check the fine print.

What happens if I can't repay after graduation?

Banks typically offer restructuring options — extended tenure, reduced EMI, or temporary moratorium extensions. Education loan defaults don't lead to immediate legal action in most cases, but they'll severely damage your CIBIL score, affecting future loans and credit cards. Communicate with your bank early if you're struggling — they'd rather restructure than write off.

Do girl students get any special benefits?

Yes. Most public sector banks offer 0.5% interest rate concession for girl students. Some state schemes offer additional fee waivers for girls in STEM courses. Check with your specific bank and the Karnataka Department of Higher Education.

Which bank is best for education loans in Karnataka?

SBI Scholar Loan has the lowest base rate and widest college coverage. Canara Bank is strong in Karnataka specifically (headquartered in Mangalore) and processes faster for local colleges. For speed, HDFC Credila is fastest but costlier. There isn't one "best" — apply to two or three and compare.

Need help finding colleges within your budget? WhatsApp +91 6363 330 233 with your KCET/COMEDK rank, category, and budget. We help you get the best admission to your preferred colleges without hassle.

Published by L K Monu Borkala, founder of OneCity Technologies — publishing Karnataka education directories since 2006, covering college admissions data since 2019 through CollegesInfo.org. Loan data sourced from bank websites, Vidyalakshmi portal, and RBI circulars. Interest rates change frequently — always verify with the bank before applying.